When you hear the term budget, do you cringe? Or rejoice? Many of us have an emotional reaction to budgeting. My mother used her budgeting endeavors as a report card. But her grades always ended up below average. This was because, while her arithmetic was A+, her commitment to sticking with her self-imposed budget numbers was not.

Mapping out a budget is crucial as you aim for the divorce settlement you want. So let's forge ahead. To make the journey easier, I suggest you set aside two things: your emotions and the past.

I encourage you to think of this budgeting endeavor as an opportunity to look straight into the present. If necessary, remind yourself that budget numbers are not about the past. They are about right now and about the foreseeable future.

Next, let's try to make this economic planning more palatable. I suggest you call the spreadsheet a "Spending Plan" rather than a budget. After all, the intention is to identify what you have to spend. And then to allocate what you have to spend, to meet your needs. After needs have been met, then attention can be given to your wants.

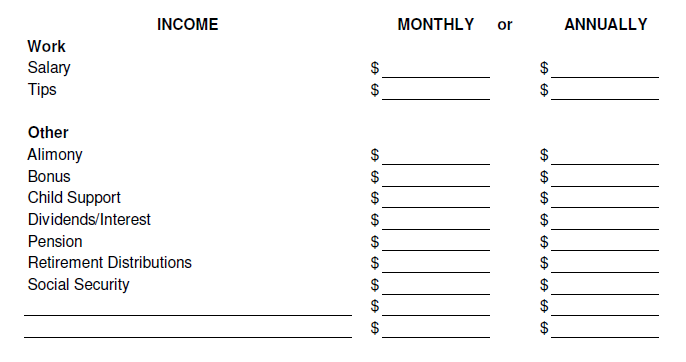

A good starting place is to have the last two or three years of tax returns handy. Take a look at all the sources of income that flow into the household. Transfer your individual income numbers from your tax returns onto your Spending Plan spreadsheet. This is your starting place.

While married, you probably filed income taxes jointly with your spouse. Going forward, this will no longer be the case. If you do not yet have individual income, leave the income entries blank until anticipated individual income amounts and/or sources are confirmed.

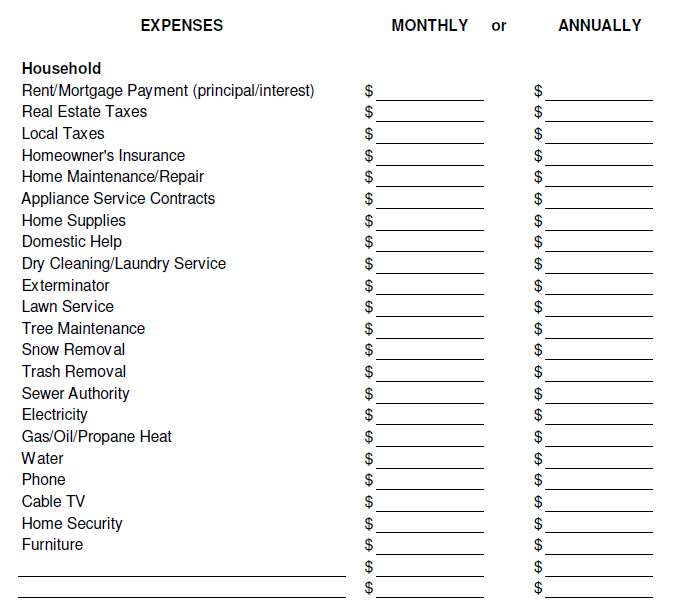

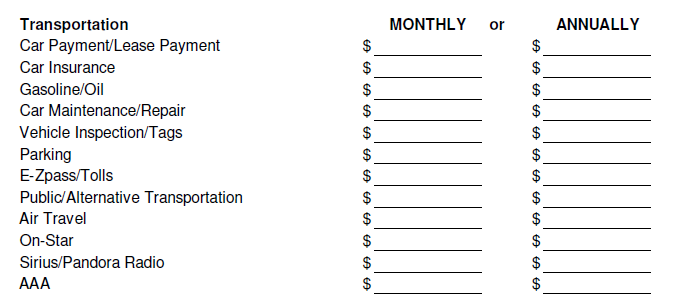

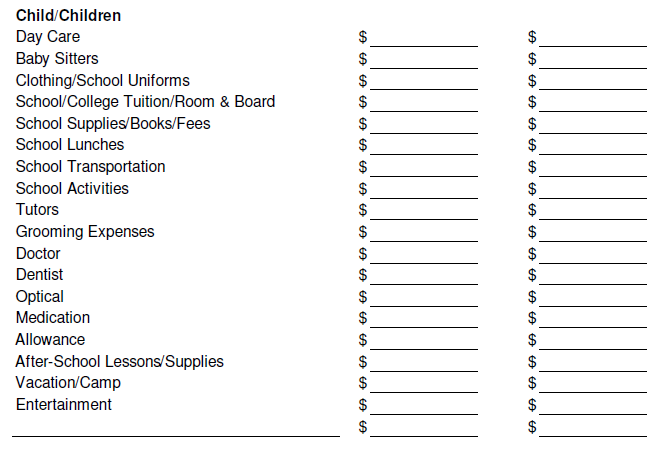

So far so good. Now the real homework begins. Take a look at every category on the spreadsheet below. Fill in each blank that pertains to your own lifestyle. Make these entries either on a monthly or an annual basis—whatever seems more user-friendly to you.

Remember you cannot just identify the monthly expenses you had while married and divide them down the middle. Going forward, when you and your ex-spouse live in separate households, each home will incur its own set of expenses. This means it will likely cost more to live post-divorce than when you were married and living under one roof.

This homework assignment will illustrate at a glance what it costs you to live. The expenses framework tells you how much you need at a minimum on a monthly basis to maintain your lifestyle after divorce. Taking the time to get the numbers right may enhance your well-being for years to come.

With that task completed, you may be ready to tackle other aspects of your divorce negotiation. If you discovered an income shortfall—now that two households require funding—it's time to "sharpen your pencil.”

"Sharpen your pencil" means to evaluate each expense and trim or eliminate any that is not essential. Generally speaking you do not want to spend down retirement savings for current income. There may not be time to replace such funds before you are ready to retire.

If you do A+ arithmetic like my mother and stick to your numbers, you may be pleasantly surprised. An excellent client of mine did both. Five years post-divorce she owns her home, loves her lifestyle, and has more retirement savings than she ever anticipated.

Download our 30-item divorce checklist.