Mijoo Lee

1 and

In Tae Hwang

In Tae Hwang

The Bank of Korea, 67, Sejong-daero, Jung-gu, Seoul 04514, KoreaDepartment of Accounting, College of Business and Economics, Chung-Ang University, Seoul 06974, Korea

Author to whom correspondence should be addressed. Sustainability 2019, 11(11), 3165; https://doi.org/10.3390/su11113165Submission received: 13 May 2019 / Revised: 28 May 2019 / Accepted: 31 May 2019 / Published: 5 June 2019

(This article belongs to the Section Economic and Business Aspects of Sustainability)Since the global financial crisis, management incentive compensation, which is sensitive to financial firms’ short-term performance, has been noted to threaten financial systems’ sustainability by incentivizing managers to pursue excessive risks. Subsequently, international standards have been established regarding compensation for financial institutions’ senior executives and employees. However, this compensation may impact not only banks’ risk-taking behaviors, but also their earnings management, as the latter affects financial performance while compensation is decided as a reflection of such performance. Therefore, this study analyses executive compensation’s impact on banks’ earnings management using compensation data on South Korean banks. The analysis revealed higher earnings management using a loan loss provision with more variable compensation. On the one hand, if the proportion of equity-linked compensation to incentive compensation increased, then earnings management increased. On the other hand, more deferred compensation led to increased earnings smoothing. This study evaluates regulatory impacts across multiple dimensions by analyzing the effects of incentive compensation standards—intended to increase financial systems’ sustainability—on individual financial institutions and further contributes to studies on managerial decision making.

The global financial crisis spurred serious questions about the sustainability of business models and operating practices among financial firms that had distributed capital in the pursuit of profits. The short-term maximization of profits had previously been justified based on efficient resource allocation, but individual financial firms’ efficient decision making failed to create stable financial systems. Causes of financial crisis include not only excess liquidity due to low interest rates and the reckless trading of derivatives to exploit asset bubbles, but also corporate governance, including remuneration systems. Remuneration for financial firms’ managers has focused on short-term performance to provide incentives, leading to an underestimation of risks of derivatives, or riskier investments [1]. The fact that the compensation structure may play an important role in banks’ risk-taking is supported by the Institute for International Finance [2], as 98% of the large international banks it surveyed agreed that compensation structures were a factor in the 2007–2008 financial crisis. Given such indications, international standards that link senior executives’ and employees’ remuneration to long-term performance and risk have been prepared to restrict financial firms’ excessive risk-taking behaviors. The standards are the Financial Stability Board’s (FSB) principles and standards on sound compensation practices which have been introduced with the aim to enhance financial systems’ stability.

However, incentive compensation may impact not only banks’ risk-taking behaviors, but also their earnings management. Accounting choice affects financial performance, and compensation is decided as a reflection of management’s performance. Therefore, managements have incentives to use accounting choices to maximize compensation. Management incentives for earnings vary depending on how accounting earnings are reflected in the incentive compensation. Hence, this study aims to analyze the executive compensation system’s impact on banks’ earnings management. Specifically, we aim to verify the impacts of variable incentive payments, the payment of bonuses in equity-linked instruments, and deferred compensation on banks’ earnings management.

The corporate governance and remuneration reports published with the introduction of the FSB’s compensation principles provided a research environment for an empirical study on the impact of financial firms’ incentive compensation on management decision making. There is no selection bias as the compensation principles are compulsorily applied to firms meeting certain criteria, and all banks, in particular in South Korea. Although these principles were also applied to some financial firms other than banks, the disclosure standards applied to financial investment (securities) and insurance businesses differed from those applied to banks. Thus, only some companies disclosed the details of deferred payments before 2014. Further, financial investment and insurance businesses have different operational details and asset compositions from those of banks, with low comparability between their accounting choices. Consequently, this study restricts its analysis to banks, as well as empirically analyses incentive compensation’s impact on earnings management using relevant data disclosed since 2010.

This study analyses incentive compensation standards’ impact on the financial system’s sustainability in terms of the sustainability of individual financial firms, with a particular focus on the reliability of accounting information. Hence, this study provides an opportunity to consider regulatory impacts across multiple dimensions by investigating the impact of compensation standards—which were established to restrict managers’ excessive risk-taking—on earnings management. This study can also help establish financial supervisory policies. Banks are mentioned as being different from other companies because of their publicness. As fund providers and intermediaries in the financial system, banks play a significant role in the economy. Kandrac [3] finds that bank failures lead to lower income and compensation growth, higher poverty rates, and unemployment. Moreover, access to capital is an essential enabler for the successful transition to economic systems that adopt innovative approaches to address the relationship between business, the environment, and society [4]. Thus, to prevent suspicious accounting and risky operations from harming economic and social sustainability, governments typically supervise financial companies to a greater extent than they do companies in other industries. Therefore, an analysis of management compensation can not only contribute to weighing up the reliability of financial data, but also to devising plans to enhance supervisory effectiveness and efficiency.

How compensation reflects accounting performance can impact managers’ earnings management incentives, which can be more prominent in banks with almost no owner-managers. This is because compensation accounts for most of the profits anticipated from managing a firm, as few profits are gained from increases in future corporate values. Therefore, an analysis of compensation’s impact on earnings management may contribute to studies on non-owner-managers’ decision making.

Compensation systems are utilized to resolve the agency problem caused by the separation of ownership and management [5,6]. The agent theory treats an enterprise as a group of contractual relationships under which the principals engage the agent to perform some service on their behalf which involves delegating some decision making authority to the agent, and defines an agent problem as the mismatch of the agent’s and principal’s interests, which does not result in the optimal allocation of resources [5]. It is difficult to monitor managers in financial firms, as ownership and management are separate and information asymmetry is noticeable due to the nature of the business [7,8]. Thus, such compensation as incentives or stock options are more actively utilized to address the agency problem [9]. Nevertheless, due to a lack of data, few studies have presented empirical evidence for incentive compensation’s impact on financial firms. Hence, this study is expected to provide useful information to financial firm investors.

This study analyzed incentive compensation’s impact on earnings management using compensation data from Korean banks’ senior executives, which was published upon the introduction of the Principles for Sound Compensation Practices and Implementation Standards enacted by the FSB. South Korea implemented the FSB’s sound compensation standards in 2009 immediately after they were established. In 2010, the FSB reported that only five participants, including South Korea, had fully implemented incentive compensation standards; among these, only three (Hong Kong, South Korea, and Saudi Arabia) had implemented equal regulations across all its banks. Thus, South Korea provides a suitable context by which to analyze the impacts of the FSB’s incentive compensation standards. Our analysis suggests that more variable compensation leads to more earnings management through loan loss provisions ( LLPs ), and as the proportion of stocks or equity-linked compensation becomes higher, earnings management will increase.

As banks have low capital ratios compared to other businesses and procure most of their operating funds from a number of unspecific depositors, banks’ poor performances can lead to economic losses for these creditors. Additionally, individual banks’ insolvency or a lack of liquidity may subsequently cause other financial firms’ inability to pay or drastically decrease asset values, eventually threatening the financial system’s sustainability. The nature of such financial institutions has led to their supervisors more often emphasizing stability and soundness rather than profitability and growth. It has been noted that since the global financial crisis, incentive compensation sensitive to short-term performance can worsen financial institutions’ stability; thus, the demand for sound governance has increased worldwide [10,11]. As a reflection of such discussions, it was suggested in the 2008 G20 Washington Summit that it was necessary to reform financial firms’ incentive compensation. The FSB then issued its Principles for Sound Compensation Practices in April 2009 [12], and Implementation Standards in September 2009 [13]. Leaders of each country at the G20 Pittsburgh Summit in September 2009 agreed to approve the FSB’s compensation principles and urge financial firms in each country to implement them. Accordingly, financial firms in South Korea were asked to abide by these principles and standards and report their implementation.

The FSB’s compensation practices require the effective governance of compensation, effective alignment of compensation with prudent risk taking, and effective supervisory oversight and engagement by stakeholders, as summarized in Table 1. The most prominent of the FSB’s compensation principles involves restricting excess risk-taking by linking compensation to performance and risk. Specifically, this purpose requires the payment of performance-based variable compensation, a certain part of which must be awarded as stocks or equity-linked compensation. Variable compensation is a non-fixed reward that is contingent on discretion, performance, or results achieved. Equity incentives are compensation plans using the employer’s shares as employee compensation. The most common form is stock options; additional vehicles such as restricted stock, restricted stock units, employee stock purchase plan, and stock appreciation rights are also used. Additionally, compensation principles provide a basis to defer compensation and restrict variable compensation in the case of non-compliance with provisions regarding the maintenance of sound capital, as well as adjust it based on risk and performance.

The Korean government prepared its Best Practices of Incentive Compensation for Each Industry by reflecting the main content from the FSB’s 2010 compensation principles, which were created according to an agreement from the G-20 Summit [14]. Later, the government established its Best Practices for Financial Firms’ Governance Structure (2014) by accepting reorganization schemes from the Organization for Economic Co-operation and Development and the Basel Committee on Banking Supervision, which have been discussed internationally. In light of this, the Act on Corporate Governance of Financial Companies (August 2016) and its Enforcement Decree (August 2017) were enacted, and consequently, the FSB’s best practices have become obligations.

The compensation principles require a large part of compensation for companies’ senior executives and specific employees to be paid as variable performance-based compensation. Further, a large part of such variable compensation, (e.g., 40%–60%) should consist of deferred payments—in principle, longer than three years considering the nature of the job—in considering the duration of the existence of risks. A majority of such variable compensation (e.g., more than 50%) should be paid in a form linked to the financial firm’s long-term performance, such as stocks or equity-linked products, thereby connecting compensation and risk. Each financial firm’s compensation committee was asked to prepare a yearly report on remuneration and publish it in the three months after the fiscal year-end so specific compensation information could be accessible in the public domain. The disclosures in these reports include the compensation decision-making process, such as its composition and primary features (deferred payment methods or criteria for distributing such compensation as cash and stocks), the compensation committee’s authority and responsibility, aggregate information regarding compensation, details of senior executives’ and specific employees’ compensation (the compensation amount during the fiscal year, such as fixed and variable compensation amounts, and the numbers of recipients, the amount and type of variable compensation, the deferred compensation and payment amounts in the current fiscal year, the retirement compensation amount, the number of beneficiaries, and the maximum amount per person).

Although FSB’s incentive compensation standards have been established to increase financial systems’ sustainability, studies have yet to empirically verify these standards’ impacts on individual financial firms’ sustainability. Sustainability occurs when compensation reinforces the activities companies take to create sustainable long-term value for multiple stakeholders. For sustainability, balance between profit and risk is required to avoid both excessive risk-taking not aligned with the business strategy, and too conservative a risk profile that diminishes the ability to provide market-competitive returns [15]. International discussions after the global financial crisis highlighted the preference for excessive risk as the greatest threat to the financial system’s sustainability, and incentive compensation standards also focused on restrictions on risk taking [16]. The standards presuppose that individual banks’ sustainability obtained by risk restriction would enhance financial systems’ stability. However, it is doubtful whether this standard motivates managers as intended since the performance measures of financial institutions are subject to short-term managerial choices.

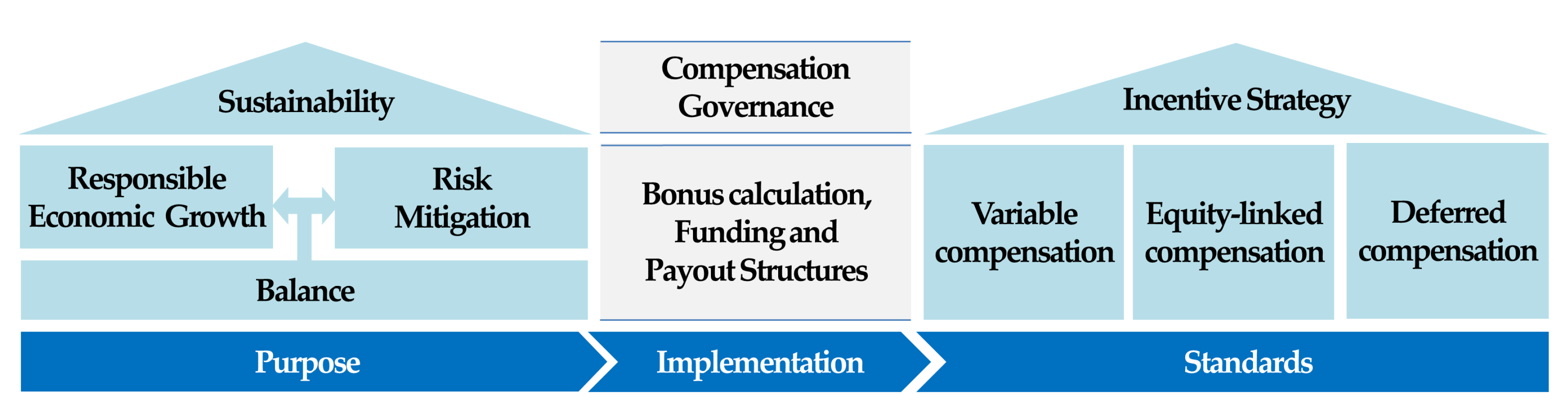

For the long-term sustainability of a firm, a compensation structure should be established, implemented, and maintained in line with objectives that prevent a shortsighted optimization and cashout, and keep investments alive. The FSB standards try to implement these objectives through bonus calculation, funding, and payout structures. Appropriate rewards allow managers to make choices that limit risk with a sustainable profit. The profitability which meets the shareholders’ required rate of return while performing the financial intermediation function that satisfies the financial service required for the real economy growth is ‘minimum profitability’. Sustainable profit is a profit considering growth and unexpected loss compensation additionally to ‘minimum profit’, and it is profitability to guarantee going-concern [17]. Regarding risk control, corporate governance and accounting transparency as well as operational risk must be considered from an integrated perspective to secure financial firms’ sustainability. Each compensation component is expected to serve a different purpose as described in Figure 1. Variable compensation drives growth and profitability, while equity incentive enhances stakeholder alignment by promoting ownership and rewarding value creation. Short-term variable incentives support annual results and near-term individual performance. Deferred (clawback) incentives drive value creation over time and increase executive accountability. Equity compensation helps ensure executive interests remain aligned with shareholder interests over the longer term [15]. However, earning and stock return are vulnerable to managerial short-term decisions such as accounting choice. Because accounting choice affects compensation, the compensation program influences accounting choice. This implies that performance-based compensation can be an incentive to produce distorted accounting information in order to maximize rewards. Lack of accounting transparency induced by compensation structures is an evidence of failure of sufficient profitability and uncontrolled risk, which damage sustainability. Because accounting transparency is one of the factors affecting the sustainability of the firm [18], the compensation structure may have both positive and negative effects on sustainability. Therefore, it is the subject of empirical analysis whether incentive compensation increases corporate sustainability or opportunistic behavior for compensation maximization.

Variable compensation links performance to compensation to ensure managers can make real efforts in maximizing corporate value. Following agent theory, the larger the conflict of interest between the principal and the agent, the greater the agent cost, and alignment of interest by compensation can be a measure to deal with agency cost [5,6]. Empirical analysis supports agent theory by showing that the presence of high foreign stakeholder or compensation committee increases the ratio of variable compensation to reduce the agency cost [19]. If variable compensation acts as a factor to enhance the corporate value, earnings management will be suppressed. However, variable compensation may cause short-term earnings management or excessive risk taking rather than maximizing long-term corporate value, depending on how the compensation is provided. Investors learn of management performance, which can measure corporate value, through the accounting information managers prepare. However, accounting information may vary depending on managers’ discretionary choices. Crocker and Slemrod [20] argue that managers’ optimum choices to maximize shareholders’ value and their candid report on performance were objectives that could not be achieved simultaneously if the managers were compensated for their own discretionally-determined performance. Cornett et al. [21] report that CEO pay-for-performance sensitivity is positively related to earnings management. Other researches also indicated that managers were likely to exercise discretion over reported earnings that would increase earnings volatility under the optimum incentive compensation structure [22,23]. Koch et al. [24] analyzed the impact of supervisory standards for incentive compensation from the Board of Governors et al. [25] on the establishment of the countercyclical capital buffer and earnings management in banks. The countercyclical capital buffer refers to the capital additionally accumulated during an economic upturn, when profits increase, to secure a loss-absorbing capacity during an economic downturn. A countercyclical provision system also exists and was applied for a similar purpose in other countries, such as Spain. This aims to reduce the business cycle’s negative impact on banks by accumulating additional provisions during the economic upturn and using such accumulated provisions during an economic downturn. The latter is matched with the expected loss calculated in considering the entire business cycle. The incentive and outcomes of securing a countercyclical capital buffer or countercyclical provision may be applied to those of earnings management, in that the loan loss allowance is frequently used in banks’ earnings management. These studies note that performance-linked bonuses provide an incentive to maximize earnings and increase compensation for the current period. Even if the next period’s reported earnings decrease for the earnings managed upward for the current period, the utility shall increase for the time value corresponding to the increased bonus in the current period. As the proportion of variable compensation increases, the expected earnings management profits increase; subsequently, variable compensation and earnings management are expected to positively correlate. Hence, the following hypothesis is established:

Hypothesis 1.The greater the proportion of variable compensation to the total compensation for bank managers, the greater the earnings management.

The earnings management incentives provided by variable compensation are expected to differ depending on the direction and size of latent earnings. On the one hand, managers under the variable compensation system have an incentive to use their maximum accounting discretion to boost earnings when latent earnings can sufficiently reach a minimum bonus threshold. On the other hand, if performance cannot reach the minimum threshold, the incentive exists to report fewer earnings in the current period to maximize the next period’s bonus, as the current period’s downward earnings management is reversed in the next period. Healy [26] analyzed earnings management behavior in a case in which managers’ compensation was primarily based on accounting earnings, and a variable incentive was provided in a certain performance range. Managers reported upward earnings within a range of incentive criteria, while they levelled earnings downward to increase the anticipated future incentives if earnings were to exceed a cap or fall short of the lower threshold. Thus, variable compensation provides an incentive to manage earnings upward—in the case of performance high enough for an incentive—or downward (the ‘big bath’) if performance is too poor for an incentive. Consequently, earnings smoothing will decrease and earnings volatility will broaden with larger variable compensation, except in the case in which latent earnings have substantially increased.

The most common method to provide an incentive, which allows the managers to make decisions to maximize corporate value, involves providing stocks or equity-linked compensation, such as stock options [27,28,29]. The large theoretical literature on optimal contract theory and traditional agent theory argue that executive compensation must be paid in line with shareholder value [27]. Empirical research provides evidence that when corporate governance is developed, most of the remuneration of executives is paid out as stock options [30,31]. If compensation linked to equities reconciles the interests between managers and shareholders, this will suppress managers’ discretionary behaviors that distort the financial reports of firms. Although various studies have discussed the effects of stock option compensation, these have failed to provide a coherent conclusion. Positive results occur [28,29,32,33,34,35], in that the provision of stock options reduces agency costs and increases corporate value. In contrast, negative results do exist to indicate that the use of discretionary accruals to manipulate reported earnings is more pronounced at firms where the CEO’s potential total compensation is closely tied to the value of stock and option holdings [36]. Researches provide evidence of an increase in earnings management immediately before exercising the option to create favorable conditions for stock options [9,37,38]. Relative to other components of compensation, stock options are associated with stronger incentives to misreport because convexity in CEO wealth introduced by stock options limits the downside risk on detection of the misreporting [39]. In the banking industry, Cheng et al. [40] find that managers with high equity incentives are more likely to manage earnings. On the one hand, if equity-linked compensation effectively reconciles managers’ and shareholders’ interests, earnings management will decrease [41]. On the other hand, if managers who have been provided equity-linked compensation increase earnings with the intent to increase the share price to maximize their own private interests, earnings management will increase. While positive effects from decision making to maximize shareholder values occur in the long-term, an immediate increase in share price appears through earnings management. South Korean banks’ managers with relatively short tenures may be more interested in short-term profits than long-term performance. Hence, the following hypothesis is established:

Hypothesis 2.The higher the proportion of equity-linked compensation to variable compensation for bank managers, the higher the earnings management .

Financial reporting impacts share prices by providing information about banks’ value. The bigger the profit, the more positive the impact it has on the stock price. Senior managers know more about the true distribution of latent earnings than investors and can sell their shares at the highest price through upward earnings management when latent earnings are at the upper end of the manager’s estimated earnings distribution. Safdar [37] argued that managers tend to increase reported earnings for an increased share price before exercising a significant amount of stock options and would exercise them at the highest share price. If managers inflate reported earnings during times of high latent earnings to maximize the share price when they sell their stocks, earnings volatility will increase. Koch et al. [24] argued that managers would sell their shares when they believed their earnings have peaked, as they have an information asymmetry over the firm’s external stakeholders related to the distribution of latent earnings; thus, equity-linked compensation would enhance the bank’s pro-cyclicality. Income-increasing earnings management raises banks’ capital ratio and overestimating the ability to make loans eases banks’ lending attitudes while expanding loans. This consequently leads to increased insolvency, which was reflected in loan loss provisions with an increasing evidence of loss during the recession. This worsens the soundness of banks’ capital, and the subsequent shrinking loans magnify the amplitude of the business cycle.

In contrast, equity-linked compensation provides an incentive to lower earnings volatility through income smoothing to positively affect share prices. Earnings management may influence share prices by helping the bank build a reputation as a low-risk, consistent performer. One primary motivation for income smoothing involves enhancing the evaluation of corporate value, as this can be observed as the discounted present value for future expected earnings, and the discount rate used to calculate this present value positively correlates with firm uncertainty [42]. Low earnings volatility can boost share prices by increasing the price earnings ratio [43]. To the extent that stock-based compensation motivates managers to demonstrate such consistent earnings performance, the manager has a strong incentive to use discretion to report consistent earnings [44]. However, as Korean bank executives’ average tenure is only two to three years, which is too short to anticipate an increase in share prices through earnings smoothing, the profits from decreasing earnings volatility are insignificant. As of the end of December 2016, the average tenure of the board of directors’ members (excluding executives appointed in the reference month) as disclosed in each bank’s governance report (annual report) was 24.3 months. Therefore, equity-linked compensation is likely to provide an incentive to restrict income smoothing, and to aggressively manage earnings upward when latent earnings are significant.

As the 2006 SEC reform required the disclosure of long-term compensation, such as deferred compensation and pensions for CEOs in the United States, studies have been conducted on the impact of ‘inside debt’ on firms’ financial activities, such as investment activities, debt contracts, and share prices. Classic agency cost of debt problems related to risk-shifting and excessive payouts should diminish in importance when managers hold large pensions or deferred compensation. Sundaram and Yermack [45] and Tung and Wang [46] reported that risk-taking incentives decreased if the ratio of inside debt to CEOs’ stock compensation was higher. Edmans and Liu [47] indicated that the use of inside debt decreased the agency costs of debt, and Wang et al. [48] demonstrated that inside debt negatively correlated with conservative accounting. Wei and Yermack [49] also noted that the share price of firms with CEOs that were paid substantial amounts of inside debt decreased, while bond prices rose when the firms disclosed their CEOs’ inside debt by following the SEC’s 2007 disclosure reform for the first time.

Inside debt’s impact on earnings management can be predicted in both directions. First, inside debt provides an incentive for managers to operate their firms conservatively [50,51]. Inside debt causes managers to operate on a profit-and-loss structure similar to creditors. Even if more reported earnings are generated due to upward earnings management, the value of inside debt, which is a residual claim, shall not increase. However, the risks caused by earnings management may decrease the value of inside debt, and therefore, inside debt suppresses upward earnings management.

Alternatively, the hyperbolic discounting theory explains human psychology, in that the ‘smaller and sooner’ reward is preferred than ‘larger and later’ reward. According to hyperbolic discounting theory [52], executives prefer being compensated in a timely manner to deferring some portion of their compensation to a later time, even if the compensation is deferred into an interest-bearing account. Applying this to compensation reveals that managers will prefer more compensation at the present time rather than in future profits. Additionally, Kahneman and Tversky [53] argued that due to the human tendency toward loss aversion, the non-utility from losses is larger compared to the utility generated from profits although the amount of gains and losses may be equal. Therefore, if managers recognize inside debt as a loss from the period’s expected compensation, they will attempt to minimize damage by receiving an incentive. This may result in upward earnings management [54].

He [55] indicated that inside debt is associated with higher financial reporting quality, and Dhole et al. [56] demonstrated that deferred compensation negatively correlated with both accrual-based and real earnings management. Koch et al. [24] argued that the deferred payment of incentive compensation and the adjustment of remuneration (malus) according to long-term performance suppressed upward earnings management. Alternatively, Byun and Lee [54] reported that an empirical analysis of the impact of the CEOs’ inside debt on earnings management in 1500 US S&P firms indicated a positive relationship between inside debt and income-increasing earnings management. Thus, inside debt may decrease earnings management, but it can also cause upward earnings management.

On the one hand, the incentive to conservatively manage banks as provided by deferred compensation has a negative impact on earnings management. On the other hand, the bonus maximization incentives provided by deferred compensation positively affect earnings management; while deferred compensation can restrain earnings adjustments, it may also lead to upward earnings management. Deferred compensation’s effect on earnings management depends on the relative size of incentives to manage earnings upward and incentives of restraints. Therefore, it is subject to empirical analysis.

Hypothesis 3. Deferred compensation’s effect on earnings management does not determine directionality .This study estimates banks’ earnings management using a loan loss provision ( LLP ). Unlike discretionary accruals, which are used to measure earnings management in non-financial firms, estimations using LLP s are advantageous as they produce relatively small estimation errors by using a single account [57], and they can clearly explain the motives of earnings management. Bank managers are known to use their discretionary power in estimating loan losses in connection with earnings smoothing, signaling, and BIS capital ratio management [58,59,60,61,62]. This study verifies not only the relationship between earnings management and incentive compensation by analyzing how banks’ discretionary LLP relates to incentive compensation, but also the relationship between earnings smoothing and incentive compensation by analyzing the relationship between earnings before taxes and provisions ( EBP ) and LLP .

The discretionary loan loss provision is a measurement of bank earnings management and is estimated using the model suggested by Kanagaretnam et al. [63] and Wahlen [64]. First, the following model regresses the loan loss provision annually on the beginning loan loss allowance ( LLA , or the reserve for bad debt), beginning non-performing loans, the change in non-performing loans, net loan charge-off, changes in total loans, and loans’ composition. We also use beginning total assets as an alternate deflator, although our results are not sensitive to this choice.

where LLP = A provision for loan losses divided by beginning total loans; BEGLLA = The beginning loan loss allowance divided by the beginning total loans; BEGNPL = The beginning non-performing loans divided by the beginning total loans; CHNPL = The change in non-performing loans divided by beginning total loans; LCO = The net loan charge-offs divided by beginning total loans; CHLOANS = The change in total loans outstanding divided by beginning total loans; LOANCATEGORIES = COMM (commercial loans divided by beginning total loans), CON (consumer loans divided by beginning total loans), RESTATE (real estate loans divided by beginning total loans), FL (foreign loans divided by beginning total loans), and SMCOMM (small and medium corporate loans divided by beginning total loans).

Second, the residual ( ε ) derived from the above Model (1) is estimated as the discretionary loan loss provision ( ALLP ). Among the model’s independent variables, the beginning LLA ( BEGLLA ) is expected to have a negative regression coefficient ( α 1 < 0). This is because a higher beginning LLA leads to a smaller LLP that should be deposited in the current period when the other conditions are identical. Further, α 2, α 3, and α 4 are expected to be positive regression coefficients. The expected loss increases with a larger BEGNPL , which increases LLP , and the amount of current LLP increases with higher changes in non-performing loans ( CHNPL ). Beaver and Engel [65] indicated that the current LCO provided information regarding the future LCO , as the LCO can influence the expectations of current loans’ collectability. Therefore, the LCO will positively correlate with the loan loss provision. Further, α 5 is expected to have a different sign depending on the incremental loans’ quality.

Although NPL and LCO are variables that measure loan risks, a significant difference exists in loan risks depending on the loan’s composition [66]. Thus, the loan composition by type was also included as a variable. For example, corporate loans have a higher credit risk than household loans, and mortgage loans have a lower default risk than credit loans. Further, small and medium corporate loans have a higher credit risk than large corporate loans. Therefore, even if the NPL or the LCO are the same size, a difference exists in anticipated future losses if the loans’ composition differs. If such a difference is not controlled, the residual from Model (1) may reflect the bank’s operational type, whether business or retail. Therefore, Model (1) includes five variables to indicate the loan composition: corporate ( COMM ), household ( CON ), mortgage ( RESTATE ), foreign currency ( FL ), and small and medium-sized enterprise loans ( COMM_SM ).

We estimate the following Model (2) to analyze the relationship between incentive compensation and earnings management:

where ALLP = discretionary loan loss provision estimated from the residual in Model (1); VARIABLE = Senior executives’ variable compensation divided by total compensation; EQUITY_LINKED = Senior executives’ equity-linked compensation divided by variable compensation; DEFERRAL = Senior executives’ deferral compensation divided by total compensation; AVGCOMP = Senior executives’ total compensation divided by the number of executives subject to disclosure; TALN = The natural log of total assets; LOANS = The total loans outstanding divided by beginning total assets; LOSSNET = An indicator variable that equals 1 if net income < 0, and 0 otherwise; PASTLLP = The prior year’s LLP divided by beginning total loans; EBP = The net income before taxes and LLP divided by beginning total loans; TIER1 = The Tier 1 risk-adjusted capital ratio at the beginning of the year; SPECIAL = An indicator variable that equals one if bank i is a ‘special’ bank (including the Korea Development Bank; the Export-Import Bank of Korea; Nonghyup Bank, established under the Agricultural Cooperatives Act; and the National Federation of Fisheries Cooperatives, established under the Fisheries Cooperatives Act), and zero otherwise; YEARCONTROLS = A year indicator variable.

Variable compensation is measured by the ratio of senior executives’ variable to total compensation ( VARIABLE ). If reported earnings increase as variable compensation increases, β 1 will be estimated as a significant, negative value. Equity-linked compensation is measured by the ratio of stocks or equity-linked compensation to variable compensation ( EQUITY_LINKED ). If the reported earnings increase as the equity-linked compensation increases, β 2 will be a significant, negative value. Deferred compensation is measured by the proportion of compensation subject to deferral in total current compensation ( DEFERRAL ). If the deferred compensation increases or decreases earnings management, β 3 will represent a statistically significant value that differs from zero. Many previous studies define managers’ ‘inside debt’ as the manager’s credit to the firm, including pensions [45,49]. However, financial firms in Korea introduced the FSB’s compensation standards at the same time following supervision by financial authorities. If inside debt is measured as the manager’s claim to the firm, deferred compensation should increase over time, and therefore, this study uses senior executives’ ratio of deferred compensation to the total current compensation in each period as a variable to analyze the deferred compensation’s impact on managers’ decision making. This creates a limitation, as this involves studying the period immediately after introducing best practices for compensation; therefore, an analysis is needed that incorporates executives’ and employees’ credits to firms after sufficient time has elapsed.

The executive’s incentive compensation is determined by the performance during the corresponding period after the fiscal year-end. It can be observed that many banks separately disclose compensation information at a later date, or list estimates and disclose actual figures in the following year as corrections, as incentive compensation has not been finalized at the time of publication of annual governance and remuneration reports (business reports). Therefore, compensation that impacts executives’ decision making is incentive compensation for prior period’s performances. This study uses prior compensation variables ( VARIABLE , EQUITY_LINKED , and DEFERRAL ) to match the compensation that impact current accounting choices.

Based on previous studies [63,67], we controlled for the following: senior executives’ average compensation level ( AVGCOMP ), the bank size ( TALN ), the size of loans ( LOANS ), the prior year’s loan loss provision ( PASTLLP ), profitability ( EBP , LOSSNET ), and the bank type ( SPECIAL ). The senior executives’ average compensation level relates to agency costs and an incentive for earnings management. As expected income by maintaining executives’ status increases with higher compensation, it can be expected that highly compensated executives will endeavor to achieve consistent long-term management performance. Alternatively, high compensation can increase the size of incentive compensation; subsequently, the incentive toward income-increasing earnings management increases to obtain higher incentive compensation. When average compensation is used as a variable, outliers or heteroscedasticity may affect the results. As the average compensation relates to the bank size, the possibility also exists that the compensation level and bank size effect will not be distinguished. We test heteroscedasticity and fail to reject the null hypothesis of homoscedasticity. Additionally, we re-estimate the coefficients using the natural logarithm of average compensation as the variable. The analytical result is similar. The bank size variable was defined as the natural log of total assets. Prior studies on the relationship between firm size and earnings management provide mixed evidence. On the one hand, it can be argued that larger firms are more likely to manage earnings downward in response to greater regulatory or political scrutiny [68], although recent studies suggest that firm size is positively associated with earnings quality because of the greater proclivity to maintain adequate internal controls over financial reporting [69]. Hence, we make no prediction regarding the coefficient’s sign for firm size [56].

Profitability was measured using the net income before taxes and LLP ( EBP ) and an indicator variable that equals one if the net income is negative, and zero otherwise ( LOSSNET ). The Tier1 capital ratio was then controlled according to previous studies [40,60,70], which posit that in the banking industry, potential regulatory intervention influences earnings management. If high leverage indicates a firm that is closer to a debt covenant restriction, then managers in more levered firms are more likely to act to boost reported income and avoid possible covenant violations [68]. Hence, we expect a positive coefficient for the capital ratio [56].

This study uses the Financial Supervisory Service’s annual bank management statistics and each bank’s financial data as published in the Financial Information Network (FINE). Senior executives’ compensation data was collected from not only annual reports on corporate governance and remuneration in bank management disclosures as published by the Federation of Banks, but also the banks’ business reports. All domestic banks in Korea were analyzed, with an analysis period from 2009 to 2016, during which individual senior executives’ compensation information was disclosed. As a highly regulated industry, there is little heterogeneity that could have unexpected effects on the results of this banking research. Therefore this study is advantageous to draw significant results with a relatively small number of samples. This study can analyze the relationship between compensation system and earnings management without selection bias by analyzing all banks in an economic environment. As the determinants of LLP differ depending on whether International Financial Reporting Standards (IFRS) were adopted, some banks that did not adopt IFRS in 2011 were excluded from the sampling, beginning in 2011 until the year in which they were introduced. Merged banks’ data was included in the analysis until the year prior to the merger. The final sample includes 99 observations of 18 banks for the 7-year period.

Table 2 illustrates the descriptive statistics of variables from the sample used in the empirical analysis. The sample’s average variable compensation ( VARIABLE ) is 0.4820, and the highest value is 0.68. The proportion of compensation linked to long-term performance ( EQUITY_LINKED ) is 0.3163, which is lower than the 50% specified in incentive compensation standards or governance code standards. Although the average proportion of deferred compensation to total compensation is 0.2015, the proportion of deferred compensation to variable compensation is 0.4157, which is higher than the 40% specified in best practices or in the governance code. The average net income before taxes and provisions ( EBP ) was 1.7% with a standard deviation of 0.8%, which indicates that Korean banks’ profitability generally stabilizes downward during the sample period. Therefore, it is unlikely that reported earnings were managed downward, as latent earnings exceeded the variable compensation payment’s upper threshold. The annual report on domestic financial firms’ governance structure (annual reports on the corporate governance structure and remuneration system) or business reports do not disclose the existence of an upper limit in the variable compensation payment criteria. Although the incentive of upward (or downward) earnings management cannot be clearly determined, it is considered that profitability exhibits a declining trend, and subsequently, it is unlikely that earnings exceeding the cap will be reported, even if caps exist. The frequency of current net loss accounted for 6% of the samples, and primarily development financial institutions (DFI), including development bank and export-import bank reported losses. Therefore, it is also unlikely that earnings were managed downward (the ‘big bath’) due to latent earnings that were lower than expected. The average beginning loan loss allowance ( BEGLLA ) is 0.0174 and the average beginning non-performing loan ( BEGNPL ) is 0.0170, indicating that the coverage ratio exceeds 100%. Therefore, banks would have been able to exercise discretion in determining the LLP , as the supervisory authorities and stakeholders would not have had a large demand for additional LLA . The average Tier 1 capital ratio is 11.1147%, or much higher than the 6% regulatory standard. The lowest figure is 7.9%, which is also higher than the regulatory standard, indicating that the motivation for earnings management to adjust the Tier 1 ratio is unlikely to be high.

Table 3 presents the results of Pearson correlation analysis. Since the relations between variables in the model are supposed as linear, Pearson correlation is presented instead of Spearman’s which assesses monotonic relationships. A positive correlation exists among incentive compensation variables ( VARIABLE , EQUITY_LINKED , and DEFERRAL ). The significant, positive correlation among these incentive compensation variables indicates that the three hypotheses are not mutually exclusive, and we include variables related to all three in our regressions. Eventually, the proportion, form, and payment method of incentive compensation should be simultaneously considered to analyze the incentive compensation system’s impact on earnings management.

Table 4 displays the results from analyzing incentive compensation’s impact on earnings management using Model (2). As the model is estimated using pooled cross-sectional data, its statistical inferences are based on standard errors clustered at firm and year levels [71]. The regression coefficient of VARIABLE was −0.0025, which was statistically significant ( p < 0.01). The discretionary LLA decreased as the proportion of variable to total compensation increased. As the increased portion or amount of compensation due to the increase in reported earnings becomes larger with a higher proportion of variable compensation, the high proportion of variable compensation may be an incentive toward income-increasing earnings management. This result is comparable to the prior studies which evidenced that the use of discretionary accruals increases executive compensation, and firm managers receiving no bonus adopt income-decreasing accruals [72]. The regression coefficient of EQUITY_LINKED is also significant and negative (−0.0012, p < 0.1), suggesting that equity-linked compensation is not an effective incentive to maximize corporate value, but a motive for income-increasing earnings management. The regression coefficient of inside debt ( DEFERRAL ) was not statistically significant; thus, the proportion of inside debt is estimated to have no impact on earnings management using discretionary LLP .

Theoretically, inside debt may act as an incentive to both increase and decrease earnings management. Thus, the insignificant relationship between inside debt and discretionary LLP derived in this study may be the result of the offset effects of increasing and decreasing earnings management. Otherwise, the fact that the inside debt as defined in this study differs from that in previous studies may impact this result. Further research will be needed to distinguish these impacts.

As earnings volatility changes as a result of earnings management, we additionally verify the above analysis using earnings volatility. Earnings volatility is an important index to indicate risk, and thus, bank managers can decrease recognized risk by decreasing earnings volatility. Therefore, it is known that bank managers smooth earnings to reduce reported earnings’ volatility. Wahlen [64] and Collins et al. [60] have found that bank managers use the discretionary loan loss provision for earnings smoothing. If the latent earnings decrease (or increase), the managers can increase (or decrease) reported earnings by decreasing (or increasing) the LLP , which reduces earnings volatility. Therefore, if earnings are smoothed using LLP , the LLP and net income before provisioning will exhibit a positive (+) correlation.

However, variable compensation or equity-linked compensation may weaken earnings smoothing of banks. Table 4 indicates that variable and equity-linked compensation act as an incentive for upward earnings management. The incentive provided by these types of compensation is expected to indicate a positive (+) relationship with earnings. The variable compensation linked to accounting profit acts as an upward earnings management incentive when latent earnings are within the scope of the bonus payout, and as a downward earnings management incentive when the bonus payout criteria are not met. To maximize equity-based compensation, it is advantageous to manage earnings upward when latent earnings reach the short-term upper threshold. Therefore, as earnings increase, upward earnings management will also increase, which will increase (or decrease) earnings volatility (or earnings smoothing).

Meanwhile, deferred compensation and earnings smoothing may positively correlate, as firms’ aversion to high risk can increase earnings smoothing. As banks’ earnings volatility is recognized as a risk indicator, managers with high risk-aversion tend to make efforts to decrease earnings volatility. Managers with large inside debt holdings are more likely to protect the value of these holdings by undertaking less risky financing and investing activities [73]. Van Bekkum [74] analyzed US banks to find that deferred compensation negatively correlated with share price volatility and the risk of failure. Bennett et al. [75] found that banks’ risk of failure decreased, and its management performance increased, with larger deferred compensation. Further, Tung and Wang [46] argued that during the financial crisis, a positive correlation existed between inside debt and banks’ management performance. Inside debt restricts operational risks which increase earnings volatility. Empirical analyses reveal that interest rate risk hedging or low-risk syndicated loans could increase if bank managers’ inside debt increased [76,77]. Although these results can be attributed to the increased risk aversion caused by inside debt, the decrease in volatility might also partially occur due to earnings smoothing. The larger the deferred compensation is, the greater the earnings smoothing. Therefore, the relationship between the compensation system and earnings management is further verified through earnings smoothing.

Accounting studies of nonfinancial firms measure earnings smoothing as the difference between net profits and operating cash flows [78]. However, if the loans expand in financial firms, the operating cash flows will decrease compared to the net income, and cash flows will increase if the deposits expand. The difference between operating cash flows and net income is not the result of earnings smoothing, but intrinsic business activity. Thus, the incentive compensation’s impact on banks’ earnings smoothing is verified using the following equation incorporating a model by Ahmed et al. [62] and DeBoskey and Jiang [79], which verifies banks’ earnings smoothing by estimating the LLP ’s impact on income volatility:

Banks can decrease reported earnings’ volatility by either decreasing LLP when latent earnings decrease, or by increasing LLP when earnings increase. Thus, managers who use discretion to smooth earnings will recognize LLP more if the EBP increases, and less if the EBP decreases, to increase reported earnings [62]. Therefore, the regression coefficient of EBP is expected to be positive ( γ 12 > 0). The variables of interest in Model (3) include the EBP*VARIABLE , EBP*EQUITY_LINKED , and EBP*DEFERRAL , which are interaction variables between the incentive compensation and EBP . If γ 1, the coefficient of EBP*VARIABLE , is statistically significant and negative in Model (3), the higher proportion of variable compensation can result in a smaller earnings smoothing. If γ 2, the coefficient of EBP*EQUITY_LINKED , is statistically significant and negative, the higher proportion of equity-linked compensation can result in smaller earnings smoothing; if γ 3, the coefficient of EBP*DEFERRAL , is statistically significant and positive (or negative), the higher proportion of deferred compensation can result in larger (or smaller) earnings smoothing.

The dependent variable in Model (3) is LLP , representing the loan loss provision, and can be used for capital management and signaling effects as well as earnings smoothing [62]. Therefore, the model includes TIER1 , which represents the ratio of beginning regulatory capital, to control the impact of capital management and signaling effects on LLP . Additional control variables affecting LLP include beginning non-performing loans ( BEGNPL ) and the change in non-performing loans ( CHNPL ). Current NPL as well as that from the previous year-end impact LLP [80]. If managers recognize the loss in a timely manner, LLP relates to the current CHNPL ; however, if they intend to delay this loss recognition, it relates to the previous NPL . Therefore, BEGNPL and current CHNPL are included as independent variables to control for both previous and current non-performing loans. Based on previous studies, loan size ( LOANS ), the bank size ( TALN ), profitability ( LOSSNET , EBP ), and the loan charge-off ( LCO )—the variables that might impact LLP —were included in the control variables [62,80,81]. We also controlled for the loan composition with an impact on the LLP .

Table 5 displays the results from analyzing incentive compensation’s impact on earnings smoothing using Model (3). Regarding the regression coefficients’ significance, the standard errors for two-way clustering were presented in the same way as in the previous analysis. The earnings before taxes and provisions ( EBP ) positively correlated with LLP ; if latent earnings are high, the LLP increases to decrease reported earnings, and if earnings are low, the LLP decreases to increase reported earnings, leading to earnings smoothing. The regression coefficient of EBP*VARIABLE was estimated as significant and negative (−1.6403), and that of EBP*EQUITY_LINKED also produced a significant, negative value (−0.3763). The regression coefficient of EBP*DEFERRAL was significant and positive (1.3876), as the positive correlation between LLP and net income increased with a larger proportion of inside debt. Thus, variable and equity-linked compensation decrease banks’ income smoothing while deferred compensation increases it, as anticipated.

Endogeneity can arise from reverse causality or omitted correlated variables in our setting. Prior research claims performance, earnings management, and corporate governance are endogenously determined [21]. If earnings management is prevalent, then the compensation committee can design compensation structures to provide executives with more inside debt compensation on the expectation that inside debt inhibits earnings management. As the variable or equity-linked compensation amounts vary depending on management performance (profitability) and the share price, it is difficult to determine whether the prior period’s variable or equity-linked compensation was predetermined by considering the level of earnings management. However, the possibility exists that the ratio of deferred compensation is predetermined by reflecting the level of earnings management; therefore, it is necessary to analyze the causal relationship after controlling for earnings management’s impact on deferred compensation to verify the deferred compensation’s impact on earnings management. Thus, this study conducts an additional analysis with two-stage least squares (2SLS) regression to consider the possibility of endogeneity. It is adopted for the estimation of explanatory variables unrelated to the residual to eliminate endogeneity that may occur if there is a correlation between the residual and the explanatory variables.

To estimate the deferred compensation variables in the first-step regression, the following are used as instrumental variables: the marginal tax rate, the change in the future tax rate, the salary increase compared to the previous period, and the rate of salary increase. As the related tax burden is deferred if the compensation is deferred, the economic benefit of deferred compensation increases with a higher personal income tax rate. Therefore, if a higher marginal income tax rate is applied to managers, the preference for deferred compensation will be higher [82,83].

Changes in the tax rate also impact managers’ preferences for deferred compensation. If the future tax rate increases, the benefits of deferred compensation decrease; conversely, if the tax rate decreases, the value of deferred compensation increases. Although the personal income tax rate and its change impact deferred compensation, they do not logically relate to earnings management and were used as instrumental variables [56]. Moreover, Cen [84] analyzed the determinants of deferred compensation to demonstrate that deferred compensation increased when cash compensation and managers’ wealth were greater. This is because the deferred payment’s benefit of tax savings increases with a decreased need for cash. Therefore, managers’ wealth and the size of cash compensation were used as instrumental variables, as they impact deferred compensation and do not logically relate to earnings management. While Cen’s [84] study measured wealth based on the change in managers’ equity value of the firm, this study measured it with the average compensation of executives subject to remuneration disclosure, in considering the availability of research data. An over-identification test for the instrumental variables’ validity indicated no correlation between instrumental variables and error terms ( p = 0.3995). Multicollinearity among the regressor variables does not have sever effects on the estimation of parameters with VIF is 1.25~5.02 (mean 2.67). The firm individual fixed effects have taken into account.

The results of the 2SLS analysis in Table 6 indicate that a significant, negative correlation exists regarding the variable and equity-linked compensation’s relationships with discretionary LLPs , but the deferred compensation’s regression coefficient exhibited no statistical significance. Therefore, it is suggested that the analysis result of Table 4 can be attributed to deferred compensation’s impact on earnings management, rather than endogeneity.

Although the variables affecting accounting choices were controlled across all possible ranges, the possibility still exists that the omitted variables correlate with both incentive compensation and accounting choices. For example, firms with high growth expectations are likely to have low inside debt incentives [45,85], and these firms are also likely to have strong incentives to engage in earnings management to avoid missing earnings benchmarks [86]. Considering this, we verify the correlation between the current incentive compensation and accounting choices. As current incentive compensation is decided in the next period, the manager cannot know the details of such compensation while preparing the current financial statements. Therefore, this implies that the relationship between current incentive compensation and accounting choices involves the impact of a variable that simultaneously influences both incentive compensation and accounting choices.

As Table 7 illustrates, current incentive compensation does not significantly impact earnings management. Therefore, the result from Table 4 has not occurred from an endogenous variable that simultaneously impacts both the compensation and earnings management. Additionally, the analysis of the relationship between the current compensation and earnings smoothing indicated no significant relationship between variable compensation and earnings smoothing, which contrasts the observation that the prior year’s variable compensation significantly reduces earnings smoothing. The degree to which the current variable compensation weakened earnings smoothing was statistically insignificant at −0.4971, but the prior year’s variable compensation (−1.6403) was statistically significant at the 1% level. Although some significant relationship exists between the current deferred compensation and current earnings smoothing, the sizes of regression coefficients and significance were smaller than those from the prior year’s deferred compensation. The regression coefficient to estimate the current deferred compensation’s impact was 0.9671, which was smaller than that of the prior periods’ deferred compensation (1.3876), and the statistical significance (at 5% level) was also lower than that of the prior year’s compensation at the 1% level. However, the impact of current equity-linked compensation on earnings smoothing did not significantly differ from the prior year’s compensation.

Additionally, we directly test whether earnings management affects compensation by analyzing earnings management’s impact on variable compensation. We find that the earnings management from both ( t − 1) and t have no significant effect on variable compensation; the results are not reported for brevity.

As the current period’s downward earnings management increases reported earnings for the next period, when it is difficult to receive bonuses in the current period, an incentive exists to decrease reported earnings from the current period to increase the next period’s bonus [26]. Variable or equity-linked compensation acts as an incentive to manage earnings downward when a net loss is incurred. We investigate whether the earnings management direction changes when net losses are reported by estimating Model (2) and including the interaction terms of the net loss ( LOSSNET ) and the compensation system ( VARIABLE , EQUITY_LINKED , DEFERRAL ). The analysis in Table 8 reveals that the result was in line with the expectations, although lower statistical significance for the coefficient estimates than in Table 4. In the event of a net loss, the relationship between the compensation system and the discretionary LLP reverses when profit is incurred. The regression coefficients of VARIABLE*LOSSNET and EQUITY_LINKED*LOSSNET were positive ( p < 0.05), and DEFERRAL*LOSSNET was not significant.

The sample with LOSSNET = 1 is clustered in the same period. As the clustering of losses may have affected the results, YEARCONTROLS was excluded from the model and it was re-verified. The verification results are similar to those including YEARCONTROLS .

When ALLP is a continuous variable, outliers may affect the results. Further, omitted variables or the non-linear relationships between variables may also have an impact. Therefore, we transform the dependent variable in Model (2) into a binomial variable to perform a logit analysis, the results of which are similar to those in Table 4.

Foreign ownership of banks has recently increased, and thus, foreign investors seeking short-term stock investment profits in addition to the FSB compensation standard may impact managerial decision making on the earnings management. Therefore, a foreign ownership variable ( foreign ) is added to Model (2) to analyze foreign ownership’s effect on banks’ earnings management, which does not reveal a significant relationship. An additional analysis was conducted using foreign ownership as a mediating variable, and consequently, foreign ownership does not significantly affect the relationship between the compensation system and earnings management.

A variety of corporate governance variables affect the compensation systems and are a significant indicator of managerial sustainability. The diversity of the board (gender, professionality, etc.) in relation to corporate governance can affect the relationship between compensation and transparency of accounting. Therefore, it is necessary to estimate the impact of these variables on compensation and sustainability. However, since the data such as the gender of executives cannot be obtained, this study does not include these variables. Other research suggests that the variables affecting accounting transparency vary depending on the corporate environment. Therefore, social context should be considered when expanding this study to verify the relationship between compensation and earnings management in other social contexts.

The incentive compensation may have an impact not only on the risk-taking behaviors of banks but also on their earnings management. This is because earnings management have an impact on financial performances while compensation is decided in reflection of the performances. Earnings management has an impact on the sustainability of individual financial firms through the reliability of financial statements. This study analyzed incentive compensation’s impact on banks’ earnings management using incentive compensations data in South Korean banks. The analysis showed more earnings management using loan loss provision with more implementation of variable compensations. If the proportion of equity-linked compensation became higher to incentive compensations, earnings management increased. On the other hand, more deferred compensation lead to increased earnings smoothing.

This result has contributed to empirical research and policy-making, in that very few accounting studies have verified the impact of various aspects of incentive compensation (such as the scope, form, and payment method) on financial firms. This study suggests that management compensation should be considered when evaluating the reliability of financial data. The results of the analysis also show that supervisory policies contents should include the bank’s compensation structure to enhance effectiveness and efficiency of supervision. Furthermore, this is a good source of documentation for other researchers interested in the subject of research on decision making of executives.

However, limitations exist, in that the subjects were restricted to banks in South Korea due to data restrictions. Therefore, future studies should broaden the analysis objective and attempt to duplicate this study’s results. The association between earnings management and executive bonus may vary depending upon the circumstances of the firm. Raithatha and Komera [87] report that the relationship between executive pay and firm performance may be absent among observation to the underdeveloped nature of institutional mechanisms and weak investor activism, for example in India. Therefore, further studies should find ways to consider the impact of the institutional environment. As incentive compensation is a major component of corporate governance, and impacts managers’ decision-making motives including accounting choices, active empirical research on this topic will contribute to improving the corporate environment.

I.T.H. developed the study concept and revised the paper. M.J.L. conducted the empirical and wrote the paper.

This paper is based on the M.J.L.’s Ph.D. dissertation. The authors thank the anonymous reviewers who have given useful comments to improve this paper.

Figure 1. Principles of compensation programs and implementation of incentive strategy. Summarized from [12,13].

Figure 1. Principles of compensation programs and implementation of incentive strategy. Summarized from [12,13].

Table 1. The Financial Stability Board’s (FSB) principles for sound compensation practices and implementation standards. Summarized from [12,13].

Table 1. The Financial Stability Board’s (FSB) principles for sound compensation practices and implementation standards. Summarized from [12,13].

Significant financial institutions should have an independent board remuneration committee.Remuneration for risk and compliance employees should be determined independent of other business areas and be adequate to attract qualified, experienced staff.

The firm’s subdued or negative financial performance should generally lead to a considerable contraction of the firm’s total variable compensation.

A substantial portion of senior executives’ variable compensation should be payable under deferral arrangements over a period of years.

A substantial proportion of variable compensation should be awarded as shares or share-linked instruments.

An annual report on compensation should be disclosed to the public on a timely basis, including: the decision-making process, the most important design characteristics of the compensation system, and aggregate, quantitative compensation information.

The firm’s failure to implement sound compensation policies and practices that parallel these standards should result in prompt remedial action.

| Variable | Mean | Std. Dev. | Min. | Median | Max. |

|---|---|---|---|---|---|

| ALLP | 0.0000 | 0.0009 | −0.0024 | 0.0000 | 0.0023 |

| LLP | 0.0075 | 0.0049 | −0.0005 | 0.0068 | 0.0294 |

| VARIABLEt− 1 | 0.4820 | 0.1025 | 0.1560 | 0.4882 | 0.6800 |

| EQUITY_LINKEDt− 1 | 0.3163 | 0.2832 | 0.0000 | 0.3495 | 0.8163 |

| DEFERRALt− 1 | 0.2015 | 0.1239 | 0.0000 | 0.2251 | 0.5551 |

| AVGCOMP | 3.5289 | 1.3699 | 1.1667 | 3.3833 | 8.4143 |

| TALN | 13.5378 | 1.2594 | 10.3737 | 13.5018 | 15.0607 |

| LOANS | 0.6478 | 0.1376 | 0.3011 | 0.6783 | 0.9747 |

| LOSSNET | 0.0606 | 0.2398 | 0.0000 | 0.0000 | 1.0000 |

| PASTLLP | 0.0078 | 0.0040 | 0.0004 | 0.0070 | 0.0221 |

| EBP | 0.0170 | 0.0080 | −0.0053 | 0.0159 | 0.0492 |

| TIER1 | 11.1147 | 1.9011 | 7.9000 | 10.8900 | 16.4700 |

| SPECIAL | 0.1414 | 0.3502 | 0.0000 | 0.0000 | 1.0000 |

| BEGLLA | 0.0174 | 0.0094 | 0.0041 | 0.0154 | 0.0673 |

| BEGNPL | 0.0170 | 0.0088 | 0.0083 | 0.0148 | 0.0615 |

| CHNPL | 0.0008 | 0.0079 | −0.0225 | −0.0002 | 0.0361 |

| LCO | 0.0076 | 0.0048 | 0.0004 | 0.0064 | 0.0350 |

| CHLOANS | 0.0738 | 0.0876 | −0.1582 | 0.0699 | 0.4636 |

| ALLP | LLP | VARIABLEt− 1 | EQUITY LINKEDt- 1 | DEFE RRALt− 1 | AVG COMPt− 1 | TALN | LOANS | LOSSNET | PASTLLP | EBP | TIER1 | SPECIAL | BEGLLA | BEGNPL | CHNPL | LCO | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| LLP | 0.1822 * | ||||||||||||||||

| (0.0711) | |||||||||||||||||

| VARIABLEt−1 | −0.1616 | −0.0221 | |||||||||||||||

| (0.1101) | (0.8284) | ||||||||||||||||

| EQUITY_ LINKEDt−1 | −0.2611 *** | −0.4146 *** | 0.4111 *** | ||||||||||||||

| (0.009) | (0.0000) | (0.0000) | |||||||||||||||

| DEFERRALt−1 | −0.2115 ** | −0.4607 *** | 0.3836 *** | 0.7797 *** | |||||||||||||

| (0.0356) | (0.0000) | (0.0001) | (0.0000) | ||||||||||||||

| AVGCOMPt−1 | 0.0548 | −0.1248 | 0.6329 *** | 0.4914 *** | 0.4973 *** | ||||||||||||

| (0.5899) | (0.2183) | (0.0000) | (0.0000) | (0.0000) | |||||||||||||

| TALN | 0.0984 | 0.1796 * | 0.1639 | −0.2397 ** | −0.2044 ** | 0.0635 | |||||||||||

| (0.3327) | (0.0753) | (0.1051) | (0.0168) | (0.0424) | (0.5326) | ||||||||||||

| LOANS | −0.0056 | −0.1299 | −0.3673 *** | 0.0643 | −0.0822 | −0.5274 *** | −0.2733 *** | ||||||||||

| (0.9563) | (0.2) | (0.0002) | (0.527) | (0.4184) | (0.0000) | (0.0062) | |||||||||||

| LOSSNET | 0.1301 | 0.6546 *** | 0.0129 | −0.1799 * | −0.2936 *** | 0.0978 | 0.1008 | −0.2111 ** | |||||||||

| (0.1993) | (0.0000) | (0.8991) | (0.0748) | (0.0032) | (0.3356) | (0.3209) | (0.036) | ||||||||||

| PASTLLP | 0.1242 | 0.6081 *** | 0.0357 | −0.3597 *** | −0.3753 *** | −0.0425 | 0.2104 ** | −0.2599 *** | 0.3415 *** | ||||||||

| (0.2207) | (0.0000) | (0.7257) | (0.0003) | (0.0001) | (0.676) | (0.0366) | (0.0094) | (0.0005) | |||||||||

| EBP | −0.0221 | −0.0068 | 0.1944 * | 0.0844 | 0.1623 | 0.0436 | −0.1289 | −0.1156 | −0.3951 *** | 0.2215 ** | |||||||

| (0.8282) | (0.9466) | (0.0539) | (0.406) | (0.1085) | (0.6681) | (0.2034) | (0.2544) | (0.0001) | (0.0276) | ||||||||

| TIER1 | −0.0786 | −0.0476 | 0.3589 *** | 0.0906 | 0.1951 * | 0.5152 *** | 0.3389 *** | −0.6772 *** | 0.1511 | 0.1665 * | −0.013 | ||||||

| (0.4394) | (0.6402) | (0.0003) | (0.3727) | (0.0529) | (0.0000) | (0.0006) | (0.0000) | (0.1354) | (0.0996) | (0.8984) | |||||||

| SPECIAL | 0.102 | 0.5575 *** | −0.2932 *** | −0.4555 *** | −0.5475 *** | −0.3041 *** | 0.2738 *** | 0.0701 | 0.3829 *** | 0.3736 *** | −0.1969 * | 0.1834 * | |||||

| (0.3153) | (0.0000) | (0.0032) | (0.0000) | (0.0000) | (0.0022) | (0.0061) | (0.4907) | (0.0001) | (0.0001) | (0.0508) | (0.0693) | ||||||

| BEGLLA | −0.0052 | 0.5174 *** | 0.074 | −0.3656 *** | −0.3676 *** | −0.1102 | 0.2305 ** | −0.0502 | 0.2323 ** | 0.7254 *** | 0.2572 ** | 0.1507 | 0.4915 *** | ||||

| (0.9596) | (0.0000) | (0.4669) | (0.0002) | (0.0002) | (0.2777) | (0.0217) | (0.6216) | (0.0207) | (0.0000) | (0.0102) | (0.1365) | (0.0000) | |||||

| BEGNPL | −0.0069 | 0.6979 *** | −0.1588 | −0.4196 *** | −0.4457 *** | −0.2851 *** | 0.2157 ** | 0.0656 | 0.4865 *** | 0.6394 *** | −0.0877 | 0.0432 | 0.6343 *** | 0.6923 *** | |||

| (0.9463) | (0.0000) | (0.1165) | (0.0000) | (0.0000) | (0.0042) | (0.032) | (0.519) | (0.0000) | (0.0000) | (0.388) | (0.6713) | (0.0000) | (0.0000) | ||||

| CHNPL | 0.0079 | 0.4129 *** | 0.021 | −0.1076 | −0.1919 * | −0.1022 | −0.0482 | 0.1844 * | 0.2808 *** | −0.0458 | −0.0524 | −0.1584 | 0.3591 *** | 0.1946 * | 0.0615 | ||

| (0.9378) | (0.0000) | (0.8367) | (0.2889) | (0.0571) | (0.314) | (0.6357) | (0.0677) | (0.0049) | (0.6527) | (0.6066) | (0.1174) | (0.0003) | (0.0536) | (0.5453) | |||

| LCO | −0.0008 | 0.0741 | −0.0255 | 0.0178 | 0.0939 | 0.113 | −0.0138 | −0.3421 *** | 0.0553 | 0.1367 | 0.088 | 0.1725 * | −0.1146 | 0.0296 | 0.0202 | −0.2255 ** | |

| (0.994) | (0.4658) | (0.8024) | (0.8613) | (0.355) | (0.2655) | (0.8919) | (0.0005) | (0.5865) | (0.1772) | (0.3862) | (0.0877) | (0.2588) | (0.7709) | (0.8425) | (0.0248) | ||

| CHLOANS | 0.0221 | 0.006 | −0.1764 * | −0.0484 | −0.1613 | −0.4112 *** | −0.2507** | 0.6087 *** | −0.0997 | 0.0668 | 0.0976 | −0.2481 ** | 0.2151 ** | 0.1223 | 0.1391 | 0.1257 | −0.2477 ** |

| (0.8282) | (0.9528) | (0.0806) | (0.6344) | (0.1106) | (0.0000) | (0.0123) | (0.0000) | (0.3262) | (0.5109) | (0.3363) | (0.0133) | (0.0325) | (0.228) | (0.1696) | (0.2151) | (0.0134) |

Notes: Parentheses are the p -value. ***, **, and * correspond to 1%, 5%, and 10% significance levels, respectively.

| Dep. Var.: ALLA | INCENTIVE | EQUITY_LINKED | AVGCOMP | Model (2) | ||||

|---|---|---|---|---|---|---|---|---|

| Intercept | −0.0001 | (−0.07) | −0.0008 | (−0.57) | −0.0001 | (−0.05) | −0.0009 | (−0.86) |

| VARIABLE | −0.0031 ** | (−2.59) | −0.0025 *** | (−2.81) | ||||

| EQUITY_LINKED | −0.0014 ** | (−2.38) | −0.0012 * | (−1.67) | ||||

| DEFERRAL | −0.0019 | (−1.56) | −0.0001 | (−0.06) | ||||

| AVGCOMP | 0.0003 *** | (4.96) | 0.0003 *** | (6.42) | 0.0002 ** | (2.5) | 0.0004 *** | (7.66) |

| TALN | 0.0001 | (1.27) | 0.0000 | (0.41) | 0.0001 | (0.53) | 0.0001 | (1.02) |

| LOANS | −0.0001 | (−0.1) | 0.0009 | (1.16) | 0.0001 | (0.07) | 0.0011 * | (1.72) |

| LOSSNET | 0.0004 * | (1.67) | 0.0003 | (0.64) | 0.0001 | (0.32) | 0.0004 | (1.51) |

| PASTLLP | 0.0156 | (0.8) | −0.0027 | (−0.11) | 0.0006 | (0.03) | 0.0013 | (0.05) |

| EBP | 0.0111 | (0.98) | 0.0084 | (0.57) | 0.0046 | (0.33) | 0.015 | (1.12) |

| TIER1 | −0.0001 * | (−1.97) | −0.0001 *** | (−2.68) | −0.0001 *** | (−5.22) | −0.0001 ** | (−2.3) |

| SPECIAL | 0.0002 | (1.05) | 0.0001 | (0.4) | 0.0002 | (0.42) | 0.0000 | (−0.16) |

| YEARCONTROLS | Y | Y | Y | Y | ||||

| N | 99 | 99 | 99 | 99 | ||||

| R-squared | 0.152 | 0.1783 | 0.1151 | 0.222 | ||||

| F-statistic | 1.46 | 1.37 | 0.99 | 2.05 ** | ||||

| ( p -value) | (0.1388) | (0.1797) | (0.4769) | (0.0169) | ||||

Notes: This table presents results from the estimation of Equation (2). The t- statistics as reported in parentheses are based on standard errors clustered at the bank and year levels. ***, **, and * correspond to 1%, 5%, and 10% significance levels, respectively.

| Dep. Var.: LLP | INCENTIVE | EQUITY_LINKED | AVGCOMP | Model (3) | ||||

|---|---|---|---|---|---|---|---|---|

| Intercept | 0.0155 | (1.64) | 0.0272 * | (1.83) | 0.0265 | (1.55) | 0.0128 | (1.08) |

| EBP*VARIABLE | −1.2533 *** | (−3.59) | −1.6403 *** | (−3.46) | ||||

| EBP*EQUITY_LINKED | 0.0312 | (0.15) | −0.3763 *** | (−4.81) | ||||

| EBP*DEFERRAL | 0.3556 | (0.67) | 1.3876 *** | (3.62) | ||||

| VARIABLE | 0.0249 *** | (2.97) | 0.0356 *** | (4.53) | ||||

| EQUITY_LINKED | −0.0013 | (−0.32) | 0.0047 ** | (2.28) | ||||

| DEFERRAL | −0.0097 | (−0.9) | −0.0253 *** | (−3.18) | ||||